Taking out a loan in Germany for a foreigner might sound a bit scary.

But actually, as soon as you get to know the German credit system, it’s not that difficult at all.

I am putting together all the valuable information in this article that I gathered during my experience since I live in Germany.

What is it like to get a loan in Germany

After my wife and I settled in Germany, we decided to buy a house in our town.

Not being able to finance everything on my own, I was in the situation to take out a credit to buy the house we found.

When we arrived in Germany a few years earlier, we decided to think strategically.

As we did not have any experience with banks in Germany, we opened our bank account with one of the local banks in our town.

We thought that it might help in the future if we ever decided to buy our property as local banks might have a better local network.

And indeed, when we bought our house, the mortgage broker from our local bank called the real-estate agent directly and confirmed the financing. This made things a lot easier for us.

We were able to move extremely fast and get the property.

Since 2016, banks and credit institutions must conduct a background check of everyone. They have to make sure no one can receive credit in Germany if there is no chance for them to pay their monthly rates.

How to use the loan calculator without speaking German >> READ HERE OUR FULL GUIDE >>

CLICK HERE for Loan Calculator Check24* >>

In this article:

Which type of credit to choose? >>

Foreigners: Additional criteria? >>

Loan calculator Germany: Best rates >>

Types of a credit in Germany

There are several types of loans. Some of them you might know, some you might be unaware of yet.

Let me introduce you to the different types of loan in this article.

Banks do make a difference in Germany what you use the loan for. Depending on the goods you are investing in, the interest rate and credit term may vary.

Obtain financing in Germany with your credit card

The most common form of financing in Germany, most people have, is their credit card (Kreditkarten).

The majority of banks work with card limits depending on your monthly income. Other banks offer prepaid credit cards.

For example most people use VISA and Mastercard credit cards.

American Express credit cards are less common. Not all card terminals accept them.

Loans taken on credit cards are usually due within a month. Some providers offer you debiting after 90 days. They will charge your checking account after that timeframe.

Need a cheap credit card in Germany? Try here: Kreditkarte Santander Consumer Bank*

Dispo credits: Another easy way to take out a loan

Banks usually offer dispo credits to account owners who have a regular income.

When you spend more than you have in your account, you can take a dispo credit [or overdraft credit] (Dispokredit).

A widespread example is: Close to the end of the month, your dishwasher machine broke. Unfortunately, you have no money left on your checking account, but you need to replace the dishwasher as soon as possible.

Using your dispo credit is very easy. You don’t have to ask your bank for permission to buy something up to a certain amount. You will automatically pay some interest rate on your dispo credit. The rate varies from bank to bank.

You won’t take out a dispo credit with your bank if you have a negative Schufa rating. There are just a few banks who offer it even if you have a negative Schufa rating. More about that later.

Installment loans

In 2020, about 6,7 million new installment loan agreements were signed in Germany). The number decreased by about 500,000 from 2019, most likely due to COVID-19.

An installment credit in Germany is a credit of a certain amount of money that private individuals can borrow.

People then repay it in equal monthly amounts at a fixed interest rate in a pre-agreed number of monthly installments.

Debt restructuring loan for credit optimization

13% of all Germans used this type of loan in 2020 for repaying another one that they have taken out previously.

Finance specialists recommend taking out debt restructuring loans (Umschuldungskredit), when you have an older credit running at a higher interest rate.

Credit in Germany for a house or property

In 2020, individuals in Germany have taken out around 1,118 billion euros in home loans. Germans call this type of credit in Germany “Immobilienkredit”.

They use it to either buy or build on a piece of land, a house or an apartment.

Credit for students

Education loans or student loans can come in handy if you want to learn a specific profession (like fashion designer). Or you need help financing your expenses during your education.

You may either have these loans as earmarked installment loans, meaning you can only use them for tuition, or they may be discretionary loans.

The second credit can be used for financing your living expenses and much more.

Credit providers Germany: When I choose what?

The big question now is when to choose which type of credit in Germany. To help you understand what type of credit is best for specific purposes, I put together some examples for each type of loan.

Credit cards in Germany

Credit cards (Kreditkarten) are suitable for your everyday expenses. Especially for costs that you can’t afford to pay right now but easily afford a few weeks later. I use my credit card mainly for some expenses like business travel.

My employer will pay back the amount I had to pay during a business trip like a rental car, hotel accommodations, food, etc.

They usually do that with my next paycheck.

Since I am not willing to pay with the money in my checking account, I use my credit card. The credit I take out on my VISA card is due within a month at a fixed date, let’s say the 25th of every month.

Dispo credits in Germany

Especially during the first months after moving to Germany, I was happy about the dispo credit (Dispokredit).

Moving was already quite expensive, and renting an apartment consumed some of my savings as well.

Our local bank already knew that we had a steady income and that a specific amount would be on our account each month.

So after some months, we received a letter that we do have a dispo credit of 1,500 euros.

Sometime later, my wife and I had to buy some essential kitchen tools. It was close to the end of the month, and we used up our checking account. Thanks to the dispo credit of 1,500 euros, we were still able to buy those things. And we did not have to ask our bank for permission.

Installment credit (Ratenkredit / Verbraucherkredit / Privatkredit)

German bankers call installment loans in Germany either Ratenkredit or Verbraucherkredit, or Privatkredit. Commonly, you can use them in the following situations:

Credit in Germany for a Car or Motorbike

Let’s say you are in a situation where you need a new car for you or your family. And you are most likely not able to pay for it in cash. Whether it’s a brand new or a used car, many banks offer to finance a car.

According to a study conducted by Statista, credits for a car (used and new) are the two most common types of credit in Germany in 2020.

Taking out credit like this is often very easy.

Many car dealerships are working together with major banks in Germany to offer that on-site service to their customers.

The verification process is also relatively simple:

You provide your data to the car dealer. He will then hand it over to the bank.

And usually, banks approve the eligibility within a few minutes.

Loan for furniture and interior

The third most used loan that people took out in Germany in 2020 is furniture and interior.

Imagine the situation when you are moving to a new home. Or you are young and move out of your parents’ house.

If you don’t have enough budget on the side for new furniture, you will need to take out a loan for that.

How to obtain financing in Germany for electronics and computers

Going to an electronic retailer in Germany and buying a new TV, a gaming console, mobile device, computer, or laptop can be expensive.

Some offer 0% interest rate deals. This allows you to take out a loan for those things.

You have to pay back the loan within several months to the bank. But you can take the new equipment with you right away.

The retailers are working with banks, and you can get a credit check in their store within a few minutes.

Debt restructuring financing in Germany for credit optimization

You have an older loan at an interest rate of 5%. And you would like to reduce your interest rate. Some banks offer specific credits that help you pay the old loan immediately and offer you a lower interest rate of i.e. 3%.

That way, you can save money. And also reduce the monthly credit charge, which can be helpful with bigger loans.

Credit for education and students

Education loans or student loans are helpful when moving to a different city to study a specific subject. If you want to study law in Germany, some universities rank better than others.

Getting a student loan can be beneficial to pay for tuition fees, living expenses, and more, especially if you have to move away from your parents.

Classic vocational training credit in Germany (BAföG)

In Germany, students are eligible for BAföG, which is the classic vocational training support organized by the state.

It’s there to help young people to complete their education regardless of their economic and social situation.

Since you are only eligible for BAföG in Germany if you fulfill some requirements, it makes sense to look at the student union website (Studentenwerk) for further details.

Credit providers Germany: Where to get a loan?

There are different places where you can get a credit in Germany.

Here is my short list:

>> Check24/TarifCheck* – Loan calculator

>> Smava* – Loan calculator

>> Santander Bank*

Classic credit providers (Kreditinstitute) are

- all banks (Banken)

- savings banks (Sparkassen)

- as well as building societies (Bausparkassen)

- and Peer to Peer credits (P2P)

The function of a credit institution in Germany is to provide the economy and the consumer with credit and manage the flow of funds.

Some specialized banks, such as mortgage banks or building and loan associations, offer only certain banking services.

Others, such as the majority of savings banks and cooperative banks, are universal banks.

These offer a mix of real estate financing, payment transactions, deposits, securities, and issuing businesses.

Their business model is more broadly based. In some cases, they can also offer more favorable construction loans.

Credits from banks (Bankkredit)

Banks are subject to strict requirements concerning their equity capital, and banks must structure their offers following the statutory requirements.

This also, and in particular, safeguards the borrower’s protective rights.

Creditworthiness plays an essential role in a bank loan.

A bank usually makes a sorrowful background check of everyone who’s asking for a loan. The longer you are with a bank, the more they know your credit history.

Also the easier it usually gets to take out a loan.

Credits from savings banks (Sparkassen)

The main difference between banks and savings banks lies in the fact that banks belong to private companies, while savings banks belong to a city or municipality.

Banks can make profits, but the goal of savings banks was to generate profits for the common good, for example, for charitable purposes. Back then, savings banks were created to give the poorer population access to credit.

Credits from building societies (Bausparkassen)

The real estate credit in Germany serves the construction, purchase or maintenance of a property. You then pay the credit in monthly installments. In principle, the building savings credit is an amortizing loan.

Building societies grant so-called building savings loans, which in turn are linked to the building savings contract.

The prerequisites for use are that the previously concluded “bauspar” contract must meet the agreed minimum savings. And the “bauspar” sum must be ready for allocation.

Anyone opting for a “bauspar” loan must use it for residential purposes.

The saver benefits from a low-interest loan because the interest rate is independent of the capital market over the entire term.

In principle, the “bauspar” loan is an amortizing loan.

They determine its amount by the difference between the “bauspar” sum and the “bauspar” credit balance. As a rule, the saver pays a regular monthly installment for interest and repayment of the loan.

The so-called P2P credits / Private credits in Germany (P2P / Privatkredite)

The P2P credits are still relatively new in Germany, and it’s not yet widespread to use them.

Privatekredite (P2P loans) are loans from private individuals to private individuals without having the intervention of a bank or credit institution.

There are some benefits for borrowers and lenders alike.

For borrowers, it might be helpful that no bank will check your credit rating.

P2P credits can be a good investment for lenders as many platforms promise a good historical return on investment.

Which requirements to fulfill to borrow money in Germany

Age

Age is an essential criterion if you want to take out a loan. You must be of legal age (18 years old) to conclude a loan agreement.

If you are too old, i.e., 65 or older, your bank may no longer grant you a loan. From the age limit, the residual debt insurance ends. To still get a loan at that age, you usually have to show other security.

Alternatively, you can name a guarantor.

Residence

If you want to take out a loan, you must also live in Germany. It is important that your main residence is in Germany. Proof can be provided either by means of an identity card, passport or a registration confirmation.

As a rule, you must also have a German bank account. You pay out the loan amount to this account. The monthly installments will also be debited from there.

Income

To determine whether one can get a loan, a mere statement of regular income alone is not enough. If only the borrower’s income is considered, this does not have a clear statement about his financial means.

For this reason, all credit institutions simultaneously consider the monthly expenses that the borrower has.

These include, among other things:

- Rent with ancillary costs

- Alimony

- Living expenses

- Installment payments for existing financing, loans and so on

Once all areas are clear, the banks determine whether or not the borrower can afford a loan.

Employment Status

The current employment relationship can be decisive for the approval of a loan. If you have a sufficient income as an employee, there are still reasons that speak against the approval of a loan.

If one is still in the probationary period as an employee, this can lead to the fact that a loan is not approved. Some banks openly point out that the probationary period must have existed in the current employment relationship in any case.

In the meantime, fixed-term employment contracts are usually no longer a problem. Banks know that fixed-term employment contracts have become common in the world of work. This should, therefore, not be a reason for refusal when taking out a loan.

Self-employed people have a somewhat more difficult time here. It is best to inquire directly with your house bank first.

For the self-employed in specific industries, there may be additional disadvantages. The construction industry is particularly affected by this.

Equity

If a borrower already has more significant equity, it is usually easier to take out a loan. Especially in the case of loans for vast sums, a certain amount of saved capital is essential.

In the case of construction financing, for example, some banks require a proven credit rating and equity capital amounting to 20 percent of the purchase price.

In the case of consumer loans for smaller sums, no equity is usually required.

Securities

You need specific collateral if you want to take out a loan for a considerable sum. An income alone is often no longer sufficient security for banks.

In such cases, credit institutions require further proof that installments can be paid in the future.

Among other things, these options are conceivable as collateral:

Life insurance (Lebensversicherung)

In the case of construction financing, credit institutions require life insurance. Life insurance provides security because it covers the remaining debt if the borrower dies before the end of the loan term.

Occupational disability insurance (Berufsunfähigkeitsversicherung)

Occupational disability insurance can also serve as collateral. If the borrower is no longer able to work, this insurance covers the loan.

Land charge (Grundschuld)

In the case of a real estate loan, it is not uncommon for banks to have a land charge entered in the land register. This allows the bank to auction off the property in the event of insolvency and use the proceeds to settle the loan amount.

Second borrower (Zweiter Kreditnehmer)

Banks can also provide additional security for second borrowers. If the first borrower becomes insolvent, the second must take over the monthly payments. An appropriate credit check is also carried out on the second person.

Guarantor (Bürgschaft)

If you need additional security for your loan, a guarantor can help accordingly. The guarantor is liable for his income and assets if the borrower can no longer pay the loan.

So it can be hard to find an appropriate guarantor because he has to take over everything in case of emergency.

Transfer of ownership as security (Sicherungsübereignung)

Typically a car financing is a secure transfer. This means that the bank owns the car until the loan is foreclosed. In the meantime, the borrower can use the vehicle.

SCHUFA entries as a reason for exclusion when granting a loan

If you want to take out a loan, banks first check whether there are entries at the “Schutzgemeinschaft für Allgemeine Kreditsicherung“. The credit agency stores information on the prospective borrower’s payment history.

It also notes which loans the potential borrower has already taken out. Schufa uses this information to calculate a score. This provides information about the creditworthiness of a potential borrower.

In addition to credit institutions, landlords, for example, can also request information about the creditworthiness status of private individuals from SCHUFA. On the other hand, as a private individual, you can also check the creditworthiness status of service providers.

This can make especially with developers or artisans with whom you have to implement more significant projects.

Which documents do you need to get credit in Germany?

These are the documents you need to submit to the credit institution if you want to take out a loan. The information they contain is essential to assess your creditworthiness.

These and, if applicable, other documents are therefore prerequisites for a loan at banks.

- Salary statements (in case of self-employed: Balance sheet or surplus income statement, business analysis)

- Employment contract

- Income tax assessment notice

- Proof of current liabilities

- Statement of assets (savings accounts, financial investments, life insurance policies, shares, etc.)

- Proof of homeownership

- For start-ups, an appropriate business plan

Credit Germany: Any additional criteria for me as a foreigner?

As a foreigner, you need to fulfill additional requirements. Those criteria are not as challenging to achieve as you might think.

As a foreigner in Germany, you need the following things and the things mentioned in the previous chapter.

- You have a residence in Germany, meaning you need to live in Germany permanently

- Have a current account with a German bank

- And you have a regular income

How long does it take to get a loan?

In Germany, there are instant credits and regular credits. Instant credits can be taken out within minutes (or at least within a day) from a bank.

Those credits are suitable for urgent situations and immediate needs.

When it comes to regular loans, clients receive, in most cases, their loan within a week after your creditworthiness got approved by your mortgage broker.

Tarifcheck* provides both types of credits via their platform. Make sure that you check your chosen loan for payout (Auszahlung) terms.

Loan Germany? Avoid these seven big mistakes:

1) Underestimate flexibility

A loan with low-interest rates isn’t always good in the long run. If you have a loan that offers free unscheduled repayments, you can still lower the cost.

If the loan company offers, you can use irregular income such as Christmas bonuses to repay the loan faster. This reduces both the remaining debt and the term of the loan.

It is also good if the loan includes the option of an installment break. In this way, expensive refinancing or overdraft facilities can be avoided.

2) Misjudge monetary demand

If you take out a loan for new furniture or a new car, for example, the loan amount is easy to determine. It is usually tricky when you want to renovate an apartment, for example. Here one knows the final costs often rarely.

When you choose an amount that is too high, you pay more interest than necessary.

You may also have to select a longer-term, which usually increases the loan amount. Borrowing too little money may require you to take out another loan.

If one needs a second loan to refinance the missing amount, this can often be very expensive. So take time to calculate how much the loan really needs to be.

3) Misjudge financial scope

If you want a favorable loan, a high income helps. The more you earn, the easier it usually is to service the installment.

Do not forget to take into account your expenses. Here they should not forget rent, insurance, alimony, and things of daily use.

Especially with high loan amounts, such as a house purchase, you should always calculate a budget. When comparing income and expenses, you should always reserve a portion for unforeseen costs.

And if there is enough left over for the loan, everything is fine.

In the case the rate is possibly too high, you can also choose a longer-term.

This will reduce the monthly installment, but the slower repayment will also incur more interest.

4) Incorrect Information

Always report precisely what can be accounted for. Make sure you do not misstate your expenses. Also, 0% financing is an ongoing loan and must be included in a new loan application.

5) Incomplete documentation

Banks must check their creditworthiness before approving a loan. This is required by law. However, you may want to withhold some private information.

Most of the time, incomplete documents submitted will result in a loan rejection. So if the credit institution wants to see bank statements, it is not helpful to blackout individual expenses.

6) Apply for a credit alone

My wife and I had applied for our real estate loan as a couple. Our bank advisor recommended this to us, as it meant we could get more favorable terms.

The bank had also assessed the financial situation of my wife, because in an emergency you would have to pay for the loan installments accordingly.

They do not take into account certain incomes, such as those of trainees, because they cannot be seized.

7) Do not pay attention to Schufa-neutral request

For many loans, a credit check is performed. You will only find out what interest rate you will receive when you get a personal offer.

In this process, the bank checks your creditworthiness with Schufa.

This does not automatically change your Schufa rating. However, if the bank accidentally communicates a wrong characteristic in the request, the request alone can already harm your score.

Therefore, to be safe, it is worthwhile to always make sure that the condition inquiry is Schufa-neutral.

What is Schufa?

In Germany, your creditworthiness is recorded and stored by Schufa Holding AG. Everyone who is registered in Germany is recorded by the largest credit agency in Germany.

The abbreviation Schufa stands for “Schutzgemeinschaft für allgemeine Kreditsicherung”. Whether one speaks of Schufa’s points, Schufa reports, or Schufa evaluations, the same is meant. It is about one’s creditworthiness.

This is taken as a measure of how reliably one meets utility bills or credit card payments. At the same time, it is estimated to what extent one can continue to do so.

Where do I need Schufa in Germany?

A Schufa report is essential if, for example, you want to open a new account. As already explained, a Schufa query is also carried out when applying for a loan.

The results from the query determine in the end how much interest one will pay for a loan. The higher the risk for the bank, the higher the interest.

In the meantime, landlords, brokers, or property managers also like to ask about this when looking for an apartment. Telephone and Internet providers are also interested in payment morale.

Where can I get Schufa’s score?

You can check your own Schufa score once a year free of charge.

To get this information, you only have to fill out a form and send a copy of your ID and a registration certificate by mail to Schufa.

However, it can take several weeks before this information is received. Banks and credit institutions have an advantage here because they receive the information very quickly from Schufa.

Find best rates using the loan calculator Germany

To find the best credit offers in Germany, we recommend using the website of Tarifcheck. If we had known about this option before we bought our house, we would have started a general inquiry there first.

Why TarifCheck / Check24?

Why you should use TarifCheck before you go to the bank to ask for a loan is quickly explained:

- Tarifcheck guarantees that all credit inquiries are made without affecting your Schufa score.

- In addition, you can get particularly favorable special interest rates online, which you usually can not get in the local bank.

- TarifCheck from Check24 is a free service. Competent credit and financial experts are available in the background to answer any questions.

Which steps to get the loan?

- Determine the desired amount of the loan and the term.

- Make a free and non-binding comparison on Tarifcheck.de. Within seconds, you will receive results that match your specifications.

- Apply for your loan free of charge directly afterward via the platform

- Confirm your identity free of charge either via Video-Ident or Post-Ident procedure

- Wait for the credit check. This does not take long with the lenders and does not affect your SCHUFA

- After approval, you can use the credit according to your wishes

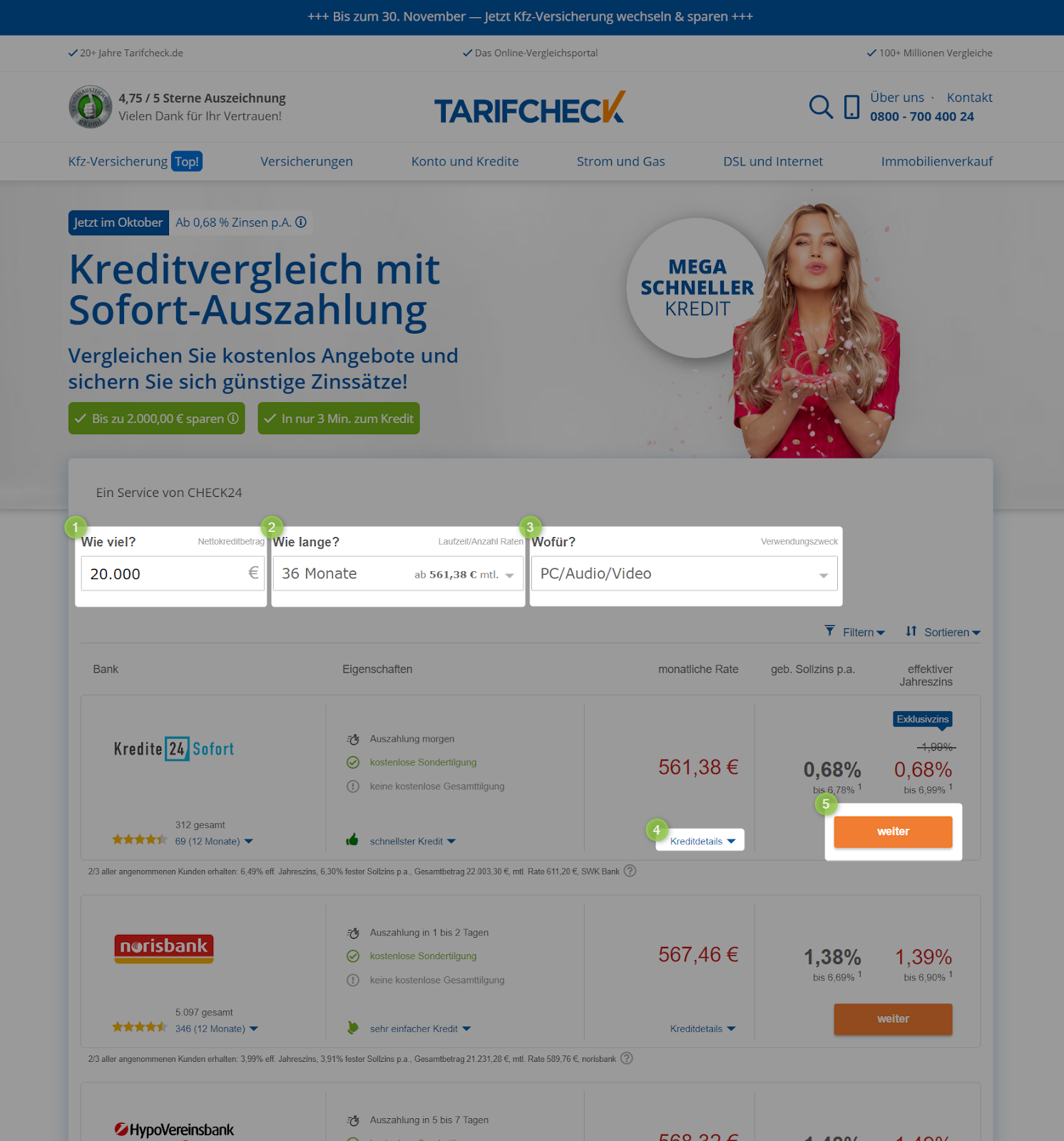

Loan calculator Germany explained

Below I have compiled the most critical steps for applying for a new loan Tarifcheck.

Step 1: Opening the website

When you open the Tarifcheck page, you can start directly by entering your first vital figures:

Enter at 1) your desired loan amount (credit amount) in euros.

Select under 2) the desired purpose (intended use). The following options are available here:

- Free use (Freie Verwendung)

- Used vehicle (Gebrauchtfahrzeug)

- New vehicle (Neufahrzeug)

- Motorcycle (Motorrad)

- Reschedule debt or pay off the existing loan (Umschuldung/Kredit ablösen)

- Settlement of overdraft (Ausgleich Dispo)

- Purchase of new furnishings or furniture (Einrichtung/Möbel)

- Modernization or construction financing (Modernisierung/Baufinanzierung)

- PC/audio/video (PC/Audio/Video)

- Travel (Reise)

In the last step, click on “Compare loans now” (Compare loans now), and you will be redirected to the next page.

Step 2: Overview of all available credit offers

You will get all available credits listed directly. You can still influence some parameters on this page. Especially about the change of the loan amount (Wie viel) under 1) or the term (wie lange) 2) they can directly influence the monthly rate (monatliche rate).

Also, the selection of the purpose of the loan 3) (Wofür) can affect the monthly rate.

If you want to learn more about the details of a loan, you can access them under 4) (Kreditdetails). Clicking on the button that says continue (weiter) will take you directly to the online application for your loan.

Step 3: Your details

After clicking on continue (weiter), you get to the first page of many where you have to answer specific details regarding your personal information.

To give you a quick overview, which required fields need to be filled out on the following pages, I put together for you the essential information after the screenshot of the first page.

- Person – Here, tarifcheck.de asks whether the credit will be covered by you or you and another person

- Anschrift – On the following page, you need to add in your current address

- Bankkonto verbinden – Please enter your banking information here to help the credit provider to send you the money and verify that you have an existing bank account in Germany

- Beruf & Haushalt – Make sure that you enter all information that can be proven regarding your profession and your household situation

- Einnahmen & Ausgaben – On this page, you have to add in all income sources and expenses that you have on a monthly/regular basis.

- Kreditoptionen – Here, you can edit some unique options regarding your credit if applicable.

Wrap-up

Even though we received all the support we needed for our real estate loan from our local bank, we would next decide to use tarifcheck.de for a credit check. The comparison options are good, and the application to take out a credit in Germany is quick and easy.

The comparison options and SCHUFA-neutral check of our creditworthiness are the reasons why we will use tarifcheck.de next time.

USEFUL INFORMATION ABOUT GERMANY

___

INSURANCE IN GERMANY

> 15 types of insurance in Germany any expat should have

___

FINANCES IN GERMANY

> How To Open a Bank Account in Germany

___

WAGES AND TAXES IN GERMANY

> Tax return Germany – Everything you need to know

> Average Salary in Germany Latest Data

___

WORKING IN GERMANY

> CV in German with Europass: How to fill in step by step

___

LEARNING GERMAN LANGUAGE

> How to learn German fast: Top 10 strategies

* The links marked in this way are affiliate links and indicate that we receive a small commission, if you decide to buy the products or services offered by our partner sites. There’s no additional cost for you. Powered by TARIFCHECK24 GmbH.