Opening a bank account in Germany is not as difficult as it seems to be.

In this article, I answer the most frequently asked questions about opening a bank account for foreigners in Germany.

I’ve put together all the mandatory information you might need if you consider living and working in Germany.

Topics in this article

Is bank account mandatory in Germany? >>

Opening a bank account as a foreigner >>

Types of banks in Germany >>

Type of bank account needed >>

Card for bank account? >>

Bank cards in Germany >>

What criteria to consider >>

Are bank accounts free in Germany? >>

Cost of bank account >>

Two or more bank accounts possible? >>

Cheapest banks in Germany >>

Best bank account in Germany >>

Safety of bank accounts in Germany >>

Documents to open a bank account >>

Can I pay with cash in Germany? >>

Can I pay by card in Germany? >>

Online payment in Germany >>

Alternative payment methods >>

Most frequent German words for banking >>

Opening a bank account online >>

How to change your bank account? >>

Closing a bank account >>

Key takeaways

- Opening a bank account in Germany is not as difficult as it seems to be.

- Hardly any employer will pay you in cash in Germany.

- Most important criteria when choosing a bank account are: local support, costs, credit cards for free

- In Germany you can pay both cash or by card. However you should always have some cash with you.

- You can choose between Sparkassen, Volksbanken, online banks (or direct banks) and mobile-only banks in Germany.

- This is the direct bank in Germany I recommend, if you’re looking for an online bank, with low or no fees:

DKB* – The direct bank Deutsche Kreditbank

How to Open a Bank Account without speaking German >> READ HERE OUR FULL GUIDE >>

CLICK HERE to open a bank account in Germany* >>

Is opening a bank account mandatory in Germany?

You might be as surprised as I was when I did my first research on how to open a bank account.

Having a bank account is surprisingly not mandatory, but it is beneficial if you have one. Hardly any employer will pay you in cash in Germany.

Even so, it’s a known issue that some construction companies tend to pay some of their foreign workforce in cash only.

As soon as you start working for a company, it’s mandatory to have a checking account with a German direct bank or savings bank.

That way, your employer can transfer your salary minus tax and other expenses like health insurance.

Salary payments by cheques also will not happen.

Can I open a bank account as a foreigner?

Yes, you can.

As previously mentioned in my introduction, opening a bank account as a foreigner is possible in Germany. You just have to prove that you have your primary residence in Germany.

But let me get into more details by providing some answers regarding the following questions.

If you have an EU passport, or on the other hand, have a resident’s permit, this process is pretty straightforward.

Bank account in Germany for non-residents: Is this possible?

You do not necessarily have to be a resident to open an account in Germany.

There is the option to open a Basis-Account (Basiskonto).

That type of account offers essential banking services, usually for free or at least for a meager fee.

But that kind of account is only valid for EU residents or people with an EU visa status.

Am I allowed to open a bank account without Anmeldung in Germany?

Yes, you are.

You can open an off-shore bank account.

You won’t need an address in Germany as a few online banks (or direct banks) and mobile-only banks in Germany allow you to open an account.

And this can be especially helpful when planning to live and work in Germany as you can organize a few things before leaving your country.

Are there any banks in Germany with English support (or other languages)?

If you need support in English or any other language from your bank in Germany.

Actually, as far as I am aware, there are currently only banks that offer English speaking customer service either by phone, their website, or email:

- Deutsche Bank

- Commerzbank

- N26 (Direct Banking)

- Targobank

What types of banks are there in Germany?

There are many different types of banks in Germany.

I want to provide you with a list of Germany’s major types of banks, based on a Wikipedia article.

Central bank (Bundeszentralbank)

The German central bank performs only governmental functions, so usually, they do not count as a public bank. They are more like a bank for the banks. Most German banks are customers of the central bank in Germany. As long as you are an individual or a company, you are referred to commercial banks.

Universal banks (Universalbank)

They deal with every kind of customer like companies, freelancers, and individuals. They offer all types of services to them.

Banks (Bank)

Major, regional, private banks, and branches of foreign banks belong to this group of banks. The term is usually used for all banks in Germany.

Savings bank (Sparkasse) and “Landesbank”

The savings banks (Sparkassen) and the “Landesbank” in Germany are banks under public law. A region, city, or town could have its own savings bank, and that type of bank is not allowed to make enormous profits for itself.

Cooperatives banks (Genossenschaftsbanken)

That specific type of bank is built up with a cooperative structure and most of the time easily recognizable by their names like “Volksbank,” “Spardabank,” or “Raiffeisenbank.”

Special banks (Spezialbanken)

Particular banks usually only conduct specific types of banking business for a small number of clients.

Bausparkassen

As a matter of fact, this particular type of “bank” in Germany is something I have already talked about when I explained to you how I bought my house in Germany. Those banks support private and public building, renovation, and purchasing properties, houses, apartments, etc.

Auto banks (Autobanken)

Those banks are in the market only for financing and leasing any kind of motor vehicle in Germany.

Which type of bank account should I have?

There are several different bank accounts in Germany that you can choose from.

To help you choose the right one, let me explain to you the different types first:

Checking account or current account (Girokonto)

This is the most common and crucial account where your salary goes in, and most of your expenses will come from. If you want to save some money or have some assets, you will have to look into one of the following accounts.

You can find a guide on finding the best current account at the end of this article.

Basic account (Basiskonto)

A basic account is very similar to a checking account. It was established for everyone, even those who do not necessarily have a monthly fixed income.

Daily deposit account or daily allowance account (Tagesgeldkonto)

Banks sometimes pay some usually low interest on your daily allowance account.

The amount of money you can use daily from this account is limited, which is why the bank pays you interest.

Fixed deposit account or time deposit account (Festgeldkonto)

With that account, you can get a higher interest based on the time you set aside your money.

You won’t be able to access your money during the timeframe except if you are willing to lose a lot of your interest rate.

Credit card account (Kreditkartenkonto)

A credit card account is only set up for your credit card.

You can either have it most of the time with your bank where you do have your checkings account or choose a separate bank for it.

Deposit account or Security account (Depotkonto)

If you are willing to buy or sell stocks and securities, you need a deposit account to do so.

You have to pay either monthly or yearly fees for that type of account most of the time.

Savings account (Sparkonto)

A savings account or “Sparkonto” nowadays is very uncommon and something from older times in Germany.

It is still offered as an account where you can store your money and get a slightly higher interest rate than a daily allowance account.

Current interest rates are at 0.1 – 0.3%, so only marginal and no longer suitable to your assets.

Do I get a card when I open my bank account?

Yes, usually, you get a giro card (EC Karte) issued by your bank specifically for your current account.

Most banks automatically offer you an additional credit card account for free.

In this case, you either get a VISA card or a Mastercard, depending on what your bank offers.

Which bank cards are most common in Germany?

The most common bank cards you will see in Germany are the giro cards (EC Karte) for your checkings account, VISA cards, and Master cards.

Less common and not everywhere accepted is American Express in Germany.

What to look for when opening a banking account in Germany?

Here are a few essential things that you should look for when you are planning to open up a new bank account:

Local support

Choose whether you need local support or whether a pure online account with a hotline is enough for your needs. A local bank, called Fillialbank, offers in-person support, while an online account provides better conditions (for example, lower or no fees).

Check the bank fees

If you need cash most of the time, make sure that you check the banks’ fees for getting money. Some banks only allow you to get cash on their ATMs without paying any fees, while the fees may differ when getting cash on other banks.

Deposit cash

Need to deposit cash regularly? If so, make sure where you can deposit cash and whether you have to pay fees for it.

Check the bank fees

The management fee for the bank account: Some banks charge a monthly or yearly fee for managing your account. Other banks do offer the same service for free. But some of those require you to have a certain income every month for getting their free service.

Check the fees for transactions

Fees for transactions: If you ever have to transfer money to other accounts or pay bills, make sure that you understand the transaction fees of your bank.

Avoid overdraft fees

The interest rate for overdrawing your account: I already wrote an article about the so-called Disposiontionskredit. If you are in a rare situation where you have to overdraft your account, be aware of the fees.

What are the interest rates

Prevailing interest rates: Only very few banks offer interest on the balance of your checkings account. Nowadays, it’s usually less than 1%.

Free of charge transactions

Girocards: Most banks allow you to withdraw money and make electronic payments for free. Just be sure to check whether that applies to your bank account as well.

Credit cards for free

Credit cards: As mentioned above, most banks issue a credit card automatically for free, and some still ask you for a fee for either a VISA or Mastercard in Germany.

When are bank accounts free in Germany?

Current bank accounts are usually free of charge in Germany when you have a monthly income above a specific amount.

That minimum monthly deposit that needs to be made in your account may vary between banks.

How much does a bank account cost in Germany?

Bank accounts can cost a monthly fee and a fee based on transactions. While direct banks are usually free, some local banks ask for a small management fee for your checkings account.

The fees are called Kontoführungsgebühren in Germany and may vary between 0 € up to 14,90 € (at Hypo Vereinsbank) at the moment.

Can I have two or more bank accounts in Germany?

There is no limit in the number of bank accounts you may have in Germany, and it is more a question of how many do make sense for an individual to have.

How to find out which the cheapest banks in Germany are?

Are you searching for the cheapest bank in Germany?

What is the best bank account?

When it comes to the question “What is the best bank account” the answer highly depends on the purpose of your account.

As you learned in the previous FAQs, there are different types of bank accounts in Germany available.

What is the best bank account for salary in Germany?

A current account/checking account or “Girokonto” is a must for a classic bank account for your salary.

The best offers in Germany for a current account are from ING and DKB, and HypoVereinsbank.

All accounts come with 0 € annual account fees and 0 € fees for credit cards.

The main difference lies in the dispo credit and the negative interest rate.

What is the best bank account for stock exchange investment?

If you want to invest in stocks, you need a different account in Germany. It’s a particular stock portfolio or securities portfolio, in German “Aktiendepot” or “Wertpapierdepot.”

Without this kind of account, you are not able to trade any stocks.

If you need a stock portfolio account, you need to take a closer look into the terms and conditions of your bank.

To open up a stock portfolio account, you first need to have a checkings account.

What is the best bank account for families?

Families and couples sometimes want to have a joint account.

This can be especially important when your spouse is on maternity leave and no longer receives maternity allowances from the state.

A joint account offers some additional benefits for couples as you get an additional ec card for free.

And your account includes both names.

In this way, you can use them for separate payments online, for example.

Some banks ask for extra annual fees or some additional fees for secondary credit cards.

Again, the best banks here are ING, DKB, and HypoVereinsbank in Germany.

What is the best bank account for kids?

Are you are thinking about opening the best bank account for kids?

It can be wise to choose a special kids or youth account, called “Kinderkonto” or “Jugendkonto.”

This is usually a regular checkings account or “Girokonto” that does have a daily limit.

Another good choice might be a prepaid credit card for kids.

The regulations for bank accounts for kids in Germany can vary between banks.

Some require your child to go to school, others need your kid to be at least 12 years old, and others won’t allow opening an account before 18.

The Bankenverband in Germany has an excellent article about this topic in general.

It can be worth having a look into one of the local banks like Sparkasse, for example.

They offer several types of accounts that are specially designed for kids.

What is the best bank account for international transfers?

Finding the best bank account for international transfers can be quite challenging for ex-pats or foreigners.

You might be in a situation where you still want the option to receive or send money in foreign currencies.

Of course, you can transfer money in every country of the world. However, it might make sense to take a closer look at transfer fees in that particular situation.

There are even special accounts for international currencies in Germany, so-called “Sofortkonten für Internationale Währungen.”

Sometimes it can make sense to work with other services like MoneyGram or Western Union.

Are you searching for the best bank account for international transfers in Germany?

Again, it makes sense to check on fees that come with international transfers first. This especially applies if you are expecting regular payments or transfers.

What is the best bank account for students?

If you are wondering which the best bank account for students could be, I recommend that you take a closer look at zero monthly fees, a credit card, and a low or no drawing credit.

Students usually do not have a regular income, and a drawing credit or “Dispositionskredit” can be beneficial.

Other benefits like free withdrawal of money and a widespread network of ATMs make sense, not only for students but for everyone.

Is it safe in Germany to have a bank account?

Having a bank account is safe for all bank customers in Germany.

All banks in Germany are protecting their customers with 100,000 Euros per account per customer.

This security is called “Einlagensicherung.”

Specific accounts are protected with 500,000 Euros per account in some cases, as the German “Bankenverband” states.

What is the guarantee in case of bankruptcy?

The “Einlagensicherung” is the guarantee that you will not lose any money in your account below 100,000 Euros per account.

This statutory guarantee is included in every German bank.

If you have more than 100,000 Euros, it does make sense to have several accounts at different banks. Split your money between those.

Are German bank accounts supervised by Finanzamt?

Tax authorities are authorized to perform automated retrieval of account information. For example, to determine income from capital assets and private sales transactions.

What documents do I need to open a bank account?

In Germany. when you plan to open a bank account, you will need a few documents.

Application form

Every bank uses some application form, and this needs to be filled out first.

Valid passport / ID

It would help if you had a valid passport. In addition to that, you will have to show them your current German residence permit.

Address

You need to provide proof of registration, proof for your address.

Initial deposit

Some banks require you to make an initial deposit – the height depends on the bank.

Proof of employment

Most banks also ask for a guarantee of employment, except those banks that allow you to open an account without a fixed monthly income.

Student visa in Germany

In case you are planning to open a student account with a bank, they also need proof of a valid student status “Studentenvisum” in Germany.

SCHUFA

Some banks also ask for an up-to-date SCHUFA credit rating.

Proof of identity

If you are opening an online account in Germany, you will be asked to verify your identity by either PostIdent. The website of Deutsche Post offers more information on that.

Can I pay with cash in Germany?

Yes, cash is usually accepted everywhere in Germany. Even so, some locations prefer payments by credit cards or your giro card.

What are the advantages of paying cash in Germany?

Like anywhere in the world, paying cash in Germany may have some advantages if you are concerned about your privacy.

Those are:

- You are staying anonymous when paying cash. Paying by card always means that you are traceable, and banks, as well as other companies, learn more about your shopping behavior

- No shop, store, restaurant, etc., may reject your cash payment. Only if you are considering paying large amounts with coins only. They may refuse payment in that case due to more efforts on their side, counting the cash

- You won’t risk that any private information like your pin code could be stolen

- Paying in cash gives you a bit of extra control over your cash flow. You are always in control that way while learning how much you can spend

- In case there is a significant energy outage, paying cash is the only option you would have to get all essentials for your daily needs

Which are the main disadvantages of paying cash in Germany?

On the other hand, there are some disadvantages as well of paying cash in Germany:

- Not everywhere, there is an ATM to get cash from. In recent times, more grocery stores offer you take out cash from your account if you shop with them to fill that gap

- More significant amounts are difficult to be paid by cash

- The states have no control over what you are spending your money on. Whether it’s about supporting a local charity or, on the opposite, a terrorist group, they won’t know where your money went.

Are there any limits when paying cash in Germany?

This refers to the maximum cash payments that are generally permitted.

In Germany, there is currently no maximum limit for cash withdrawals.

However, anyone wishing to pay contributions over €10,000 in cash must show identification.

The merchant must record and retain the details.

Where can I withdraw money in Germany?

You are always able to withdraw money from ATMs.

As previously mentioned, at some ATMs, you might have to pay a specific fee to get cash. But that highly depends on the bank you choose.

The other option to take out cash from your account is shopping at grocery stores like REWE.

They offer you to take out money if you spend more than 10 Euros during shopping at one of their stores.

What are the banks with the most ATMs?

The top 3 banks with the most ATMs across Germany are:

Sparkasse

Sparkasse and 1822direkt (they belong to Sparkasse) have around 24,000 ATMs across Germany

Volksbank

Volksbanken and Raiffeisen banks offer around 19,450 ATMs across Germany where you can get cash without having to pay any fees

In total, there are around 58,000 ATMs in Germany.

What are the fees for money withdrawal from ATMs in Germany?

The typical fees for cash withdrawal from ATMs vary between 1,95 euros up to usually 5 Euros per transaction.

Independent ATM providers may set their prices even higher depending on the location of their ATMs.

The median is at 4,22 Euros per withdrawal at the moment.

Can I pay by card in Germany?

Yes, you can pay by card in most stores, shops, grocery stores if you’d like.

But some businesses will not accept payments by card in Germany, like:

- local producers of vegetables

- traveling traders or merchants

- market stalls

- or food trucks.

Also, some smaller restaurants won’t accept card payments, but those are most likely just a few.

What are the advantages of paying by card in Germany?

There are, of course, some advantages of paying by card in Germany as well.

- You do not have much cash in your pockets, and your payment is secured by either a pin code or other type of verification (like a fingerprint on your phone)

- Payments by card are saver because usually, you have some protection from your bank

- Card payments are contactless, which is vital during a pandemic

- It’s more convenient as most banks allow you to use payments with your mobile device via Apple pay, Google pay or other services like Samsung pay or Garmin pay

- Paying with your credit card allows you to spend money even if you don’t have money in your account as the banks usually take that money out of your checkings account within four weeks after payment

Which are the main disadvantages of paying by card in Germany?

Aligned with the advantages of paying by cash here you can find the main disadvantages of paying by card in Germany:

- You are traceable. Banks and other companies alike (by getting data from your bank) will know what, when and where you buyed which type of goods

- You are more at risk of losing the overview of your cash flow. So you have to keep track of your expenses even more

- Cards can be hacked either by manipulated ATMs or by gathering data from your contactless payment options that come with most cards nowadays

Are there any limits when paying by card in Germany?

The limit entirely depends on the disposal or availability limit of your card.

The height of the daily limit may vary from bank to bank and even amongst accounts. Important factors are:

- Your monthly income

- How much money do you have in your savings account

- How well your bank knows you

- What kind of credit history do you have with your bank

Is online payment typical in Germany?

In general, you can say that online payment is more common in Germany than you might think.

During the COVID pandemic, there was a considerable shift in payment behaviors amongst Germans, and many were staying at home and considering shopping online instead of visiting a store.

Different types of common payment forms in Germany are broadly used besides paying by credit card.

What is SEPA?

SEPA stands for “single euro payments area,” also called “Lastschriftverfahren” or “Überweisung,” and allows transactions within the European Union.

So no matter whether you buy in France, Portugal, Greece, or Germany, SEPA payments work in each of those countries online.

What is IBAN?

The “international bank account number” is a unique identifier for a single bank account.

It is used again across Europe to ensure payments reach their desired destination safely.

Other countries like Switzerland, Hungary, Lichtenstein, and Norway use the IBAN as well.

What is TAN?

The TAN or “transaction authentication number” is used as a single-use password.

Some banks still issue generated TANs on paper that they ask you to enter as soon as you’d like to confirm a transaction to an external account.

Most banks nowadays use TANs generated on your mobile device or a physical TAN generator that works with your giro card.

Do I need a German mobile phone number to do online banking in Germany?

Not necessarily, but it is beneficial if you’d like to use any mobile banking applications.

Those usually accept all mobile phone numbers from various countries as you will have to verify your account anyway, either in person or by PostIdent.

How long do online bank transfers take in Germany?

Online bank transfers from one account to another usually take 1 day at max.

Most banks even transfer the money on the same day if you request a transfer before noon.

If you shop online and pay by SEPA transfer, the payment is accepted by online stores within seconds, and your order will be placed.

Which alternative payment methods are there used in Germany?

Besides the classic online payment methods, a few alternative payment methods are widespread in Germany.

What is Giropay?

Giropay is an internet payment system established in Germany.

It is based on your online banking that allows you to securely transfer money via direct online transfers to any vendor who accepts that type of payment.

If you’d like to read more about it, you can dig deeper into this payment method on Wikipedia.

Money will be transferred in a similar process like a regular bank transfer to the vendor. The money goes directly from your current account to the account of the online store.

What is Paydirekt?

To ease the process of Giropay, banks started to accept paydirekt. Once you register for paydirekt in your online banking account, you can simply use a username and password for every transaction.

The advantage is that some merchants even provide discounts if you use that payment method.

The advantage for you is that paydirekt covers every online purchase, so in case a merchant does not deliver, their buyer’s protection covers you.

Are there other payment methods accepted in Germany?

Yes, there are even more payment methods that online merchants widely accept.

Paypal might be the most established one in the market, but there are also Google Pay and Apple Pay, taken by some of the merchants.

Are there any online payment options that send you an invoice after you receive the order?

Yes, there are a few standard payment options that you can use for your online orders.

The way it works is quite simple:

The merchant receives an order, and in case either KLARNA, PayPal, or Afterpay accept you, those will cover the payment until you receive your order.

Then you will not have to pay the vendor directly, but one of the payment providers I mentioned.

They will reimburse the vendor and chase you in case you haven’t paid in time.

What are the most frequent German words I need when it comes to banking?

- Bankleitzahl = bank identification code or number

- Zahlungsart – payment method

- Zinsen – interest

- Konto – account

- Unterschrift – signature

- Formular – form

- Geldautomat – ATM

- Geld überweisen – transfer money

- Deposit money – Geld einzahlen

- Geld abheben – withdraw money

- Bitte geben Sie Ihre Geheimzahl / PIN ein – Please enter your personal identification number PIN

- Bitte geben Sie Ihre Karte ein – please insert your card

- Kontoauszug – bank statement

- Überweisung – transfer

- Abhebung – withdrawal

- Einzahlung – deposit

- Dauerauftrag – standing order

- Bargeld – cash

- Kreditkarte – credit card

- EC Karte – debit card or giro card

- Bankleitzahl (sometimes abbreviated as BLZ) – bank code number

- International Bank Account Number (IBAN) – Internationale Bankkontonummber (IBAN)

- Kredit – loan. Learn more about different types of loans here: (LINK TO last articles about taking out a loan in Germany)

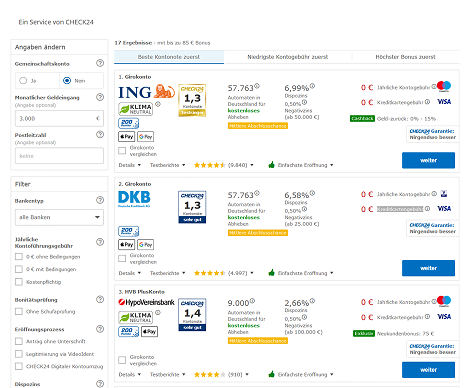

How to open a bank account online? (Girokonto)

The easiest and best way to find the best option for you for a bank account is to use the Tarifcheck* platform.

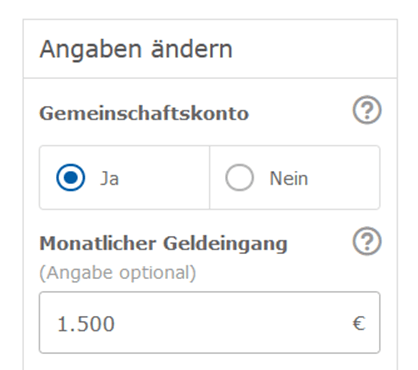

Go to their website and add in all information that you’d like to provide.

Neither your monthly income (Mtl. Geldeingang in €) nor your zip code (Postleitzahl) is mandatory for receiving a list of the best bank accounts in Germany.

It can be helpful to add in the zip code if you search for a direct bank that has a local branch in your town or near your home.

Click on the blue button that says compare now (Jetzt vergleichen).

The following page offers you a list of all bank accounts.

At 1) you can add in additional information or specify your requirements to an account to filter the list.

2) lists the best rating of the account offering first, while 3) lists the accounts with the lowest monthly fee. If you are in for a bonus for signing up a new account at a bank, you should use the filter at 4).

If you found your best suiting offer, make sure to click on 5) to move one step further.

You are asked to add in your personal information that the bank will need to verify your data on the following pages.

How to change your bank account?

Changing an existing bank account sounds stressful and complicated, but it is not.

Many banks offer a free account switching service. Just make sure that you look for either one or both of the following terms: “Kontowechselservice” and “Konto-Umzugsservice.”

Since 2016 banks have been required to work together by law and exchange all critical information amongst others.

Your new bank will inform all payment partners you worked with during the past 13 months of the bank accounts change.

What are the implications of changing your bank account?

Some implications for changing your bank account can be for example:

- an unexpected increase in fees

- deterioration of the service

- it would be best if you had a local bank, and you are moving somewhere else where your bank has no local branch

- your bank does not offer free credit cards

- interest rates are higher at another bank than at your bank

How to close your bank account in Germany?

If you consider leaving Germany again after some time, there is no need to keep your German bank account forever.

It may even cause further trouble in the future.

Also, it may make sense to keep your account for a few more months until all obligations that you have in Germany are sorted out.

If you let the account continue, you have to reckon that the charges will exceed the credit balance at some point.

Or a credit card charge can no longer be honored in total, and the bank will then cancel the account.

Anyone who wants to re-enter the country or live here after years may face legal action from creditors and a negative Schufa report.

Wrap-up

As you can see, it’s not as difficult as it sounds to get a German bank account when you consider moving to Germany for a longer time.

If you search for a good bank account, I recommend you to use Tarifcheck* first to get the best available offers in Germany for a new bank account.

USEFUL INFORMATION ABOUT GERMANY

___

INSURANCE IN GERMANY

> 15 types of insurance in Germany any expat should have

___

FINANCES IN GERMANY

> Find Best Rates for Loan in Germany

___

WAGES AND TAXES IN GERMANY

> Tax return Germany – Everything you need to know

> Average Salary in Germany Latest Data

___

LEARNING GERMAN LANGUAGE

> How to learn German fast: Top 10 strategies

* The links marked in this way are affiliate links and indicate that we receive a small commission, if you decide to buy the products or services offered by our partner sites. There’s no additional cost for you. Powered by TARIFCHECK24 GmbH. Awin affiliate partner.