Private liability insurance is the most popular non-mandatory insurance in Germany.

It is even ahead of car insurance in Germany. This is “only” used by 81% of people over 18.

Over 48 million people in Germany had private liability insurance in 2021.

I only found out about this insurance when I had already lived in Germany for a few years.

During a conversation with colleagues, we came to talk about this topic. And they were surprised and almost worried that I had not yet taken out liability insurance in Germany.

My German colleagues recommended that I take out one as soon as possible.

Admittedly, I was a little nervous myself after my colleagues told me all about it.

When I finished my work, I went home and took out private liability insurance through Tarifcheck* that same day.

After that, I felt much better. And I was reassured. 😊

Key takeaways

1) The private liability insurance is the most important non-mandatory type of insurance in Germany.

2) Liability insurance in Germany covers (almost) all types of damage you cause.

3) In addition to liability insurance – Haftpflichtversicherung, there are different names for this insurance in Germany.

4) The liability insurance is not compulsory. However, the law obliges you to pay for the damage you cause.

5) You need liability insurance in many cases in Germany. The most common ones: you accidentally injure someone, or lose the keys of your rented flat, or damage expensive electronic equipment, etc.

6) However, there are some situations that liability insurance does not cover in Germany.

7) The cost of liability insurance in Germany starts at 24 euros per year for single people.

8) The best way to get liability insurance is to use a liability insurance calculator.

Topics in this article

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

CLICK HERE for liability insurance calculator Tarifcheck* >>

First, I tried to understand everything about private liability insurance in Germany

Shortly after talking to my colleagues, I started researching everything I could about private liability insurance. I wanted to inform myself first before I would take out a new insurance policy.

And as with many other insurances in Germany, there is a wide choice of private liability insurances.

As a matter of fact, you can find over 260 personal liability insurance rates in the insurance calculator Tarifcheck* at the moment.

For instance, even the consumer center in Germany advises everyone to take out private liability insurance.

Otherwise you have to pay by law in unlimited amount for his caused damage.

To be honest, I feel that without this insurance, the existence of my family and me could be threatened very quickly.

What is precisely the personal liability insurance in Germany?

But what exactly is private liability insurance?

Private liability insurance covers (almost) all damage you cause. It doesn’t matter if it’s a mobile phone you accidentally stepped on or if you lose your flat key in an apartment building.

Furthermore, private liability insurance covers you if you have carelessly or recklessly broken something or even caused an accident.

It also covers the issue of gross negligence.

To be protected against high claims for damages, you take out private liability insurance.

What are the German names for private liability insurance?

As I learned in the conversation with my colleagues, not everyone calls private liability insurance “private liability insurance”.

Colloquially, German use the following terms:

- Privathaftpflicht

- Haftpflichtversicherung

- Haftpflicht

- Privathaftpflichtversicherung

Is private liability insurance mandatory in Germany? Does the law require it?

As I found out during my research, private liability insurance is not mandatory insurance in Germany. But I highly recommend it, as it covers almost all cases of damage.

However, the law obliges you to pay with all your assets for damages you have caused. Insurances like car insurance are mandatory in Germany. And this as soon as you want to use a motor vehicle of any kind on the road.

How many people do have liability insurance in Germany?

Back then, I wondered how many people have such insurance.

Today, in 2021, statistics show that around 48.44 million people in Germany aged 14 and over have taken out private liability insurance.

And it covers about 83% of the German population. So the question arises why some don’t take out this type of insurance.

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

Am I among the people who need liability insurance in Germany?

How do you determine if you need private liability insurance? Similar to other insurances, there are various reasons why you should take out such an insurance:

You own a house or land and rent it out, or it is not yet developed

Animal owners of, e.g., dogs or horses, which can cause personal injury or property damage

If you install an oil tank in on your property

When you are a builder yourself

If you own either a sailboat, motorboat, surfboard, or model airplane

Whether you work in the public sector, and your employer may have a right of recourse against you

Or you are a hunter

If you meet one of these cases, you should take out liability insurance. But even as a regular employee, with or without a family, enough can happen to you in life that makes liability insurance worthwhile.

Do I need third-party liability insurance for work?

Private liability insurance is also essential for employees.

And here are some typical insurance cases:

- You lose the key to your work, and they have to replace an expensive locking system

- When you accidentally transmit confidential electronic data to someone, and the company suffers a significant financial loss as a result

- Or you accidentally give the wrong advice to a customer, and the customer suffers a loss as a result

- Violations of image or personal rights also occur time and again

- Personal injury and property damage also happen frequently when you have increased contact with customers.

Also, as an employee in the public service, you should take out such liability insurance. Even if your employer is liable for you at first.

They can make recourse claims against you later.

Should I have liability insurance when I rent an apartment?

As I learned through my research, private liability insurance is also beneficial if you live in an apartment for rent.

So many things can happen in everyday life, in the worst case unintentionally causing expensive damage to the rented apartment. And the landlord can hold you liable for this.

If you have taken out liability insurance, the insurance company will:

- either examine your case

- and defend you

- or pay for the damages

There are more and more landlords who attach importance to the liability insurance of the tenant.

They demand proof of insurance (in German: Versicherungsnachweis) even before you have signed the tenancy agreement.

But don’t be worried: the German Tenants’ Association points out that such a clause in the lease is not allowed.

However, landlords can always choose another tenant who meets or wants to meet their requirements. Therefore it is advisable to take out liability insurance.

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

Do short-time tourists need liability insurance in Germany?

No, as a tourist, you don’t need to have private liability insurance. Nevertheless, even as a tourist in Germany, you can be held fully liable for any damage you cause.

If you are only in a country for a few days or a few weeks as a vacationer something like this will most probably not happen.

However, you will certainly feel better if you take out appropriate insurance as a guest or tourist.

Then I had to find out what personal liability insurance in Germany covers

With all this background, it was even more apparent that I should take out private liability insurance.

In the meantime, I had understood why I needed private liability insurance. Nevertheless, I wanted to learn more about when insurance can help me.

Typical situations covered by private liability insurance in Germany

Personal injury due to an accident

An example: You are a cyclist and ride out of a traffic-calmed area onto a cycle path. In doing so, you collide with an oncoming cyclist. After the collision, this cyclist hits his head on the asphalt and suffers serious injuries.

After fracturing his skull, the cyclist remains paraplegic. Since he was on his way to work, the Employer’s Liability Insurance Association came to you with recourse claims.

For the commuting accident, this relates to monthly costs, among other things.

Claim: 8.1 million euros

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

Loss of keys at work

Another example: The company you work for has its office in a large office building. You accidentally lose the key to the office. As a result, the entire locking system has to be replaced. In addition, the landlord requires you to pay this yourself and sends you a bill.

Damage claim: 10,000 euros

Property damage to the borrowed camera

You borrow a camera from an acquaintance for your vacation. Unfortunately, you drop it on the floor due to carelessness. As a result, the camera and the lens are irreparably damaged and the acquaintance wants a replacement for the borrowed camera.

Damage claim: 2,500 Euro

As you can see, these are only a few examples of possible cases of damage. Once you have taken out private liability insurance, you do not have to pay for the damages and costs yourself.

In minor cases this is not a problem, but in the case of a traffic accident or, for example, a building fire, it can quickly cost several million. If you don’t have insurance, your financial existence would be threatened by claims for damages.

Examples about third party liability insurance in Germany from Check24

You are covered with a personal liability policy for the following three categories of damage according to Tarifcheck*, a company of Check24.

Property damage (Sachschaden)

You accidentally tip beer over a friend’s smartphone during a movie night. The resulting damage amounts to 500 euros.

The insurance will either pay for the repair or replacement of the device.

Personal injury (Personenschaden)

Due to carelessness, you cause an accident with a cyclist crossing a street, and the cyclist breaks his thigh. After the accident, the insurance covers hospital and household costs as well as compensation for pain and suffering totalling 75,000 euros.

Loss of keys (Schlüsselverlust)

You live in an apartment building and lose the front door key. The central locking system must therefore be replaced.

Depending on the tariff, the private liability insurance covers the costs for replacing the complete locking system of approx. 1,900 euros.

What coverage amount (Deckungssumme) is recommended?

It is advisable to choose a sum insured of at least 10 million euros.

Personal injuries, in particular, can quickly result in high costs. Be it because of:

- rehabilitation measures

- compensation for pain and suffering

- conversion of an apartment to make it suitable for a disabled person

- or payment for loss of service

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

Which additional coverage is practical?

If you are considering taking out personal liability insurance, make sure that the following additional benefits are included in the best-case scenario:

Damage caused by courtesy due to unpaid assistance

Damage that occurs, for example, when you help a friend paint an apartment or when you look after the children of a family friend

Loss of keys

Loss of keys (personal or professional) is also not included in every personal liability policy.

Indemnity coverage

Another example: Let’s say you are involved in an accident that was not your fault and the person who caused the accident does not have private liability insurance. With this additional benefit, your insurance company will pay for the damage.

Damage that occurs during a tenancy

Here, damages to the building or inventory of vacation homes, hotels, and borrowed, rented, or leased property are covered.

Damage during voluntary work

Personal injury and property damage are covered if you are voluntarily active in an association in your free time.

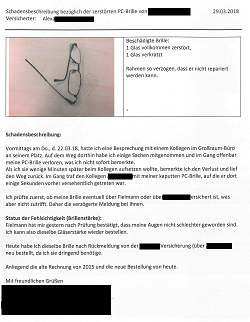

How I used my liability insurance after stepping on a colleague’s glasses (true story)

And speaking of liability insurance: A few years after taking out personal liability insurance, exactly such a case occurred that my colleagues had warned me about. Not a serious case, but it was helpful to have liability insurance.

One day, while sitting with one of my colleagues at his desk to go through some presentations, I must have accidentally knocked his glasses off the table.

This would not have been a big deal if I had noticed it right away.

Because of the carpeted floor at work, and ended our conversation after a few minutes. So as to be able to stand up better, I rolled my desk chair back a bit. In doing so, I stepped on his almost new varifocals.

Very embarrassing for me, but fortunately, the liability covered the current value of the glasses.

He had bought his varifocals new at the optician a few months ago. The new price of the glasses was around 1200 euros cost. I was lucky that my insurance had taken 100% of the property damage in this case.

I also researched what is not covered by liability insurance in Germany

Before I would take out private liability insurance, I wanted to know which damages would not be covered by it.

What situations are not covered by German personal liability insurance?

There are some damages for which liability insurance does not cover in a private environment.

We’re talking here about damage caused:

- to a co-insured person or my property

- intentionally

- by my animal, e.g., my dog (or horse)

- when you use a motor vehicle, aircraft, or watercraft

- utilizing a drone (partly covered in premium tariffs)

- by an amateur hunter while hunting

Which risks are covered by separate insurances?

Some of these claims are covered by separate insurance policies. There are the following liability insurances that cover such cases:

- Household insurance (Hausratsversicherung)

- Tierhalterhaftplfichtversicherung (Animal owner liability insurance)

- Jagdhaftpflichtversicherung (Hunting liability insurance)

- Car insurance in Germany (KFZ-Versicherung)

- Diensthaftpflichtversicherung (official liability insurance)

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

I then had to make sure the liability insurance also covered my family in Germany

Since I was married and already had a child, I wanted to make sure that my family was also covered with this private liability insurance policy.

Does the personal liability insurance in Germany cover my family, spouse, children, or partner?

So I checked whether it was possible to take out private liability insurance for the entire family or whether this benefit had to be paid separately.

In Germany, it is common for private liability insurance policies not to cover family members automatically.

Therefore, as soon as you live with your partner or have children, it is worthwhile to take out family liability insurance instead of personal liability.

Some private liability insurance policies already include partners and children. It is therefore essential to check this in advance.

Children are insured up to 18 or until they have finished their education or studies and are single.

For partners, a separate application must be made from time to time.

Does the third-party liability insurance cover other people in my life in Germany?

With private liability insurance, other persons are not insured.

Family liability insurance (Familienhaftpflichtversicherung), relatives with whom you live in the same household are usually also insured.

Does the private liability insurance cover my pets in Germany?

No, pets such as dogs are not covered by private liability insurance. For this purpose, there is a separate animal owner liability insurance (Tierhalterhaftpflichtversicherung).

Eventually, the cost for liability insurance in Germany didn’t scare me

What surprised me a lot was that the prices for private liability insurance are not that high.

Since this insurance is crucial for the entire family, I did not think twice when taking out the policy.

How much is personal liability insurance in Germany?

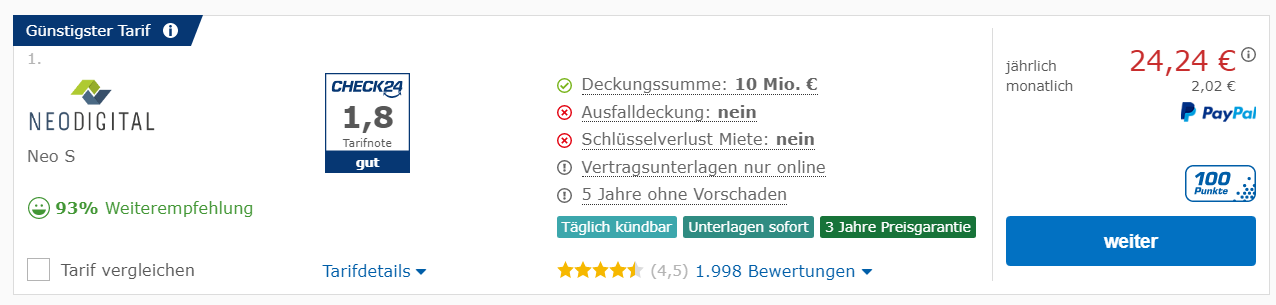

This can be easily answered: Private liability insurance is available for singles from just over 24 euros a year.

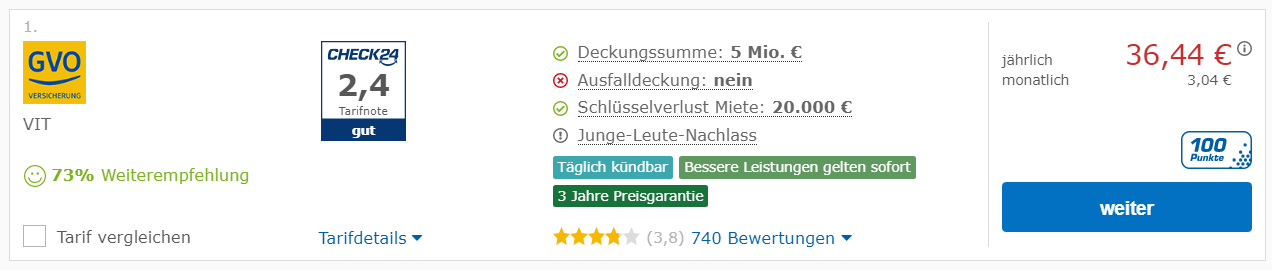

With families, the rates are somewhat more expensive and start at around 36 euros per year.

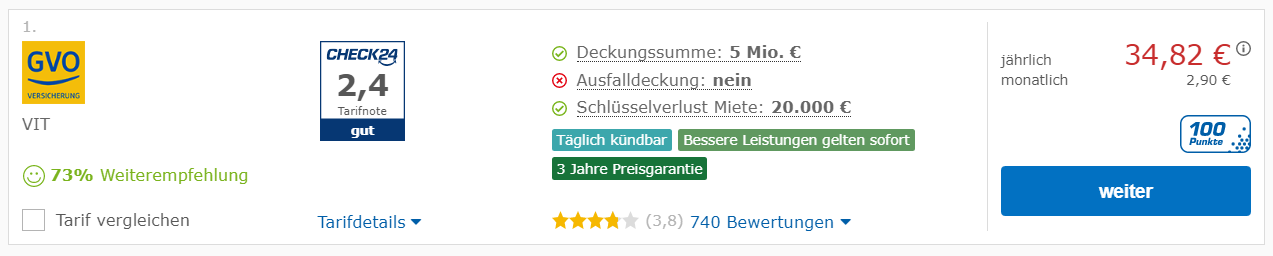

A few examples of costs from the liability insurance Germany calculator Tarifcheck / Check24

Cheap rates for singles

If you want to find cheap private liability insurance as a single, there are rates between 24.24 euros and 181 euros per year.

With a monthly payment, this is just 2.02 euros per month for the cheapest tariff.

How to use the liability insurance calculator without speaking German >> READ HERE OUR FULL GUIDE >>

Cheap Rates for Families

Favorable family rates for liability insurance start from only 36.44 euros per year currently.

The most expensive tariff can cost up to 246 euros a year.

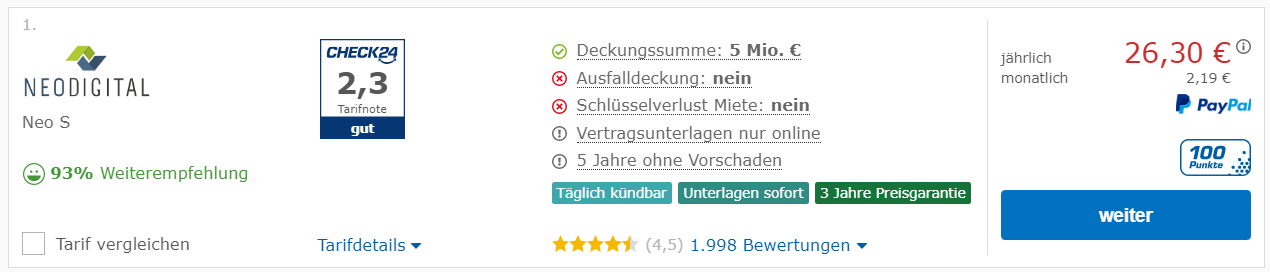

Cheap partner tariffs

For a tariff you and your spouse are covered, the annual costs start at 26.30 euros. The most expensive offer is 213 euros per year.

Favourable rates for single parents

If you are a single parent, insurance rates for private liability insurance start from 34.28 euros per year. The most expensive rate is 227 euros per year.

How to pay less with the help of the liability insurance Germany calculator

With the private liability insurance comparison from Tarifcheck*, you can save significantly with the proper settings.

You should only ensure that the desired tariff covers the desired amount of coverage and additional services such as loss of keys.

Over the configurator, for private liability insurances on Tarifcheck*, one can sort completely simply the results.

If you set the sorting to lowest price first (Lowest price first), the cheapest rates are displayed first.

How I took out the liability insurance using the liability insurance calculator Tarifcheck*

The search for the correct insurance rate was correspondingly easy on Tarifcheck*. Thus I have summarized for you here how I found my private liability insurance policy.

Step 1: Open the insurance calculator

The first step should be to open the right page of Tarifcheck* (from Check24) on the subject of personal liability.

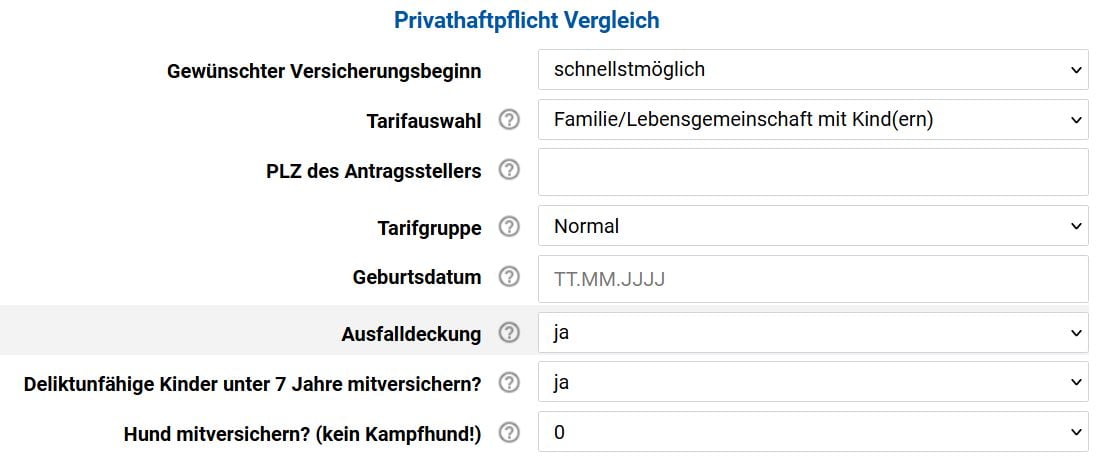

And the first information you have to offer is your family situation (Familienstad).

Here, you can choose between:

- Paar/familie – couple/family

- Single

Make your choice and click on the blue button – Jetzt Haftpflichtversicherungen vergleichen (Compare now) – to continue.

Step 2: Information about yourself

On the following page, you will need to provide additional information about yourself.

First, you have to answer following questions:

- Gewünschter Versicherungsbeginn – Desired start date of insurance

- Tarifauswahl – Rate selection

- PLZ des Antragsstellers – Zip code of the applicant

- Tarifgruppe – Tariff group

- Geburtsdatum – Date of birth

- Ausfalldeckung – Default coverage

- Deliktunfähige Kinder unter 7 Jahre mitversichern? – Do you insure children under 7 years of age who are incapable of committing a tort?

- Hund mitversichern? (kein Kampfhund!) – Do you insure a dog? (no fighting dog!)

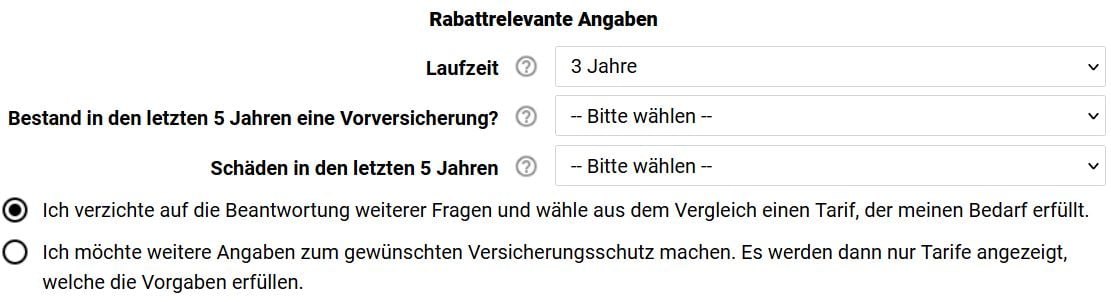

And then answer the second set of questions.

These are options that could reduce the cost of the policy (Rabattrelevante Angaben):

- Laufzeit – Duration

- Bestand in den letzten 5 Jahren eine Vorversicherung? – Did you have prior insurance in the last 5 years?

- Schäden in den letzten 5 Jahren – Damages in the last 5 years

Once you have made the appropriate selection, you can choose not to answer to the detailed questions (Ich verzichte auf …).

All you have to do is to click on the blue button “Berechnen” (calculate, compare).

Or you can choose to answer the detailed questions:

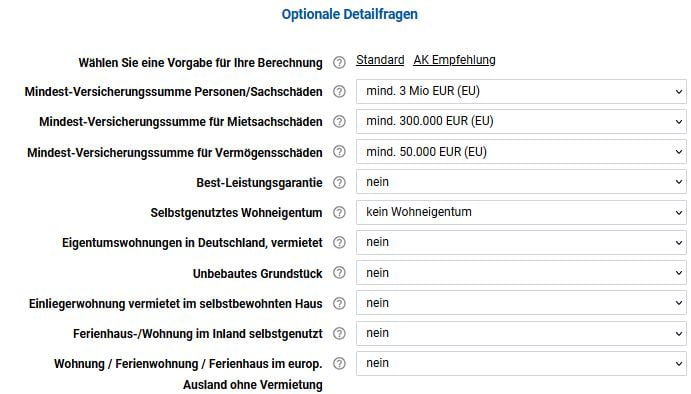

- Wählen Sie eine Vorgabe für Ihre Berechnung (Select a default for your calculation)

- Standard AK Empfehlung (Standard AK recommendation)

The minimum sum

- Mindest-Versicherungssumme Personen/Sachschäden (Minimum sum insured for personal injury/property damage)

- Minimum sum insured for rental property damage (Mindest-Versicherungssumme für Mietsachschäden)

- Mindest-Versicherungssumme für Vermögensschäden (Minimum sum insured for property damage)

- Best-Leistungsgarantie (Best Performance Guarantee)

Your property

- Selbstgenutztes Wohneigentum (Owner-occupied residential property)

- Eigentumswohnungen in Deutschland, vermietet (Condominiums in Germany, rented)

- Unbebautes Grundstück (Undeveloped property)

- Einliegerwohnung vermietet im selbstbewohnten Haus (Granny apartment rented in owner-occupied house)

- Ferienhaus-/Wohnung im Inland selbstgenutzt (Vacation home/apartment in Germany owner-occupied)

- Wohnung / Ferienwohnung / Ferienhaus im europ. Ausland ohne Vermietung (Apartment/vacation home/vacation home in other European countries, not rented out)

- Fachpraktischer Unterricht (Laborarbeiten) (Practical training (laboratory work))

- Hüten eines fremden Hundes/Pferdes (Herding of another person’s dog/horse)

Different damages

- Einschluss Öltankhaftpflicht (Inclusion oil tank liability)

- Allmählichkeitsschäden (Gradual damage)

- Gewässerschaden-Risiko, z.B. Farben (Water damage risk, e.g. paints)

- Schäden durch häusliche Abwässer (Damage caused by domestic sewage)

- Schäden durch elektronischen Datenaustausch/Internetnutzung (Damage due to electronic data exchange/Internet use)

- Gefälligkeitsschäden (Damage caused by courtesy)

- Gemietete oder geliehene Sachen (Rented or borrowed property)

The loss of keys

- Schlüsselverlust, fremder privater Schlüssel (Mietwohnung) – Loss of keys, third-party private key (rented apartment)

- Loss of keys for central locking system (no own damage) – Schlüsselverlust für Zentrale Schließanlage (keine Eigenschäden)

- Schlüsselverlust von fremden Dienstschlüsseln – Loss of keys for third-party service keys

- Weltweite Deckung gewünscht (Standard ist Europa oder EU) – Worldwide coverage desired (standard is Europe or EU)

Taking care of others

- Alleinstehendes Elternteil im Haushalt lebend – Single parent living in household

- Ehrenamtliche Tätigkeit – Voluntary activity

- Tätigkeit als Tagesmutter – Activity as a childminder

- Regressansprüche von Sozialversicherungsträgern von mitversicherten Personen – Recourse claims from social insurance carriers of co-insured persons

Other types of property, activities, objects

- Bauherrenhaftpflicht am Haus oder Grundstück – Builder’s liability on the house or property

- Eigene Surfbretter – Own surfboards

- Besitzen Sie Hunde, Pferde, Rinder, landwirtschaftliche Tiere? – Do you own dogs, horses, cattle, agricultural animals?

- Benutzen Sie eigene Wasserfahrzeuge? – Do you use your own watercraft?

- Besitzen Sie Modellflugzeuge, Ballone oder Drachen? – Do you own model airplanes, balloons or kites?

- Besitzen Sie privat genutzte Drohnen? – Do you own drones used for private purposes?

- Gehen Sie auf die Jagd? – Do you go hunting?

- Betreiben Sie eine Photovoltaikanlage? – Do you operate a photovoltaic system?

- Rechtsschutz zur Ausfalldeckung – Legal protection for default coverage

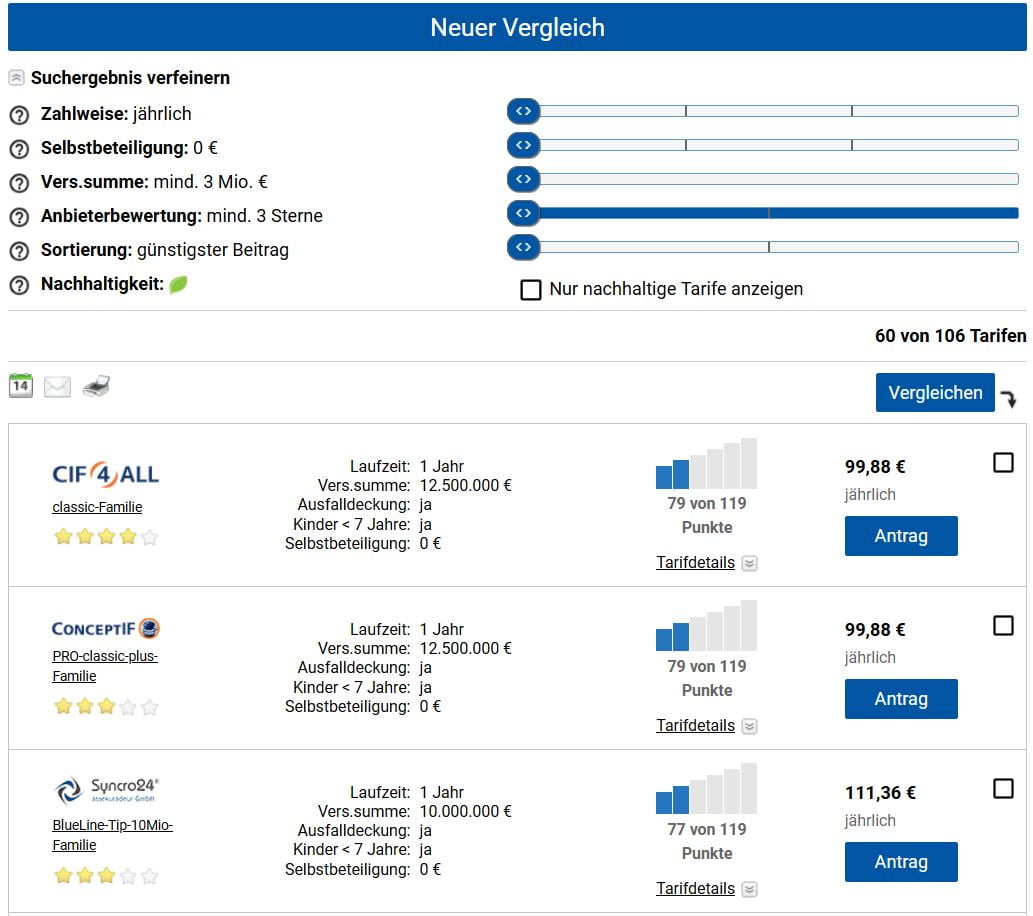

Step 3: Offers’ overview

In this view

- the individual criteria of the search can be adjusted.

- The highest tariff is the policy that offers the lowest monthly premium

- You can choose from more than 100 offers

Once you have found your desired rate, you can select it by clicking on Antrag (contract) and purchase insurance.

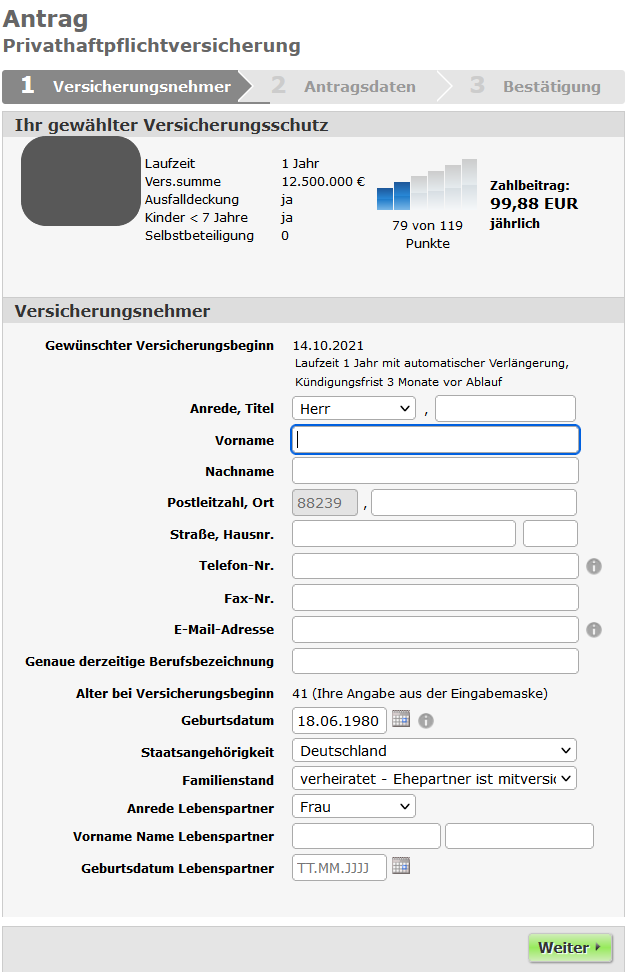

Step 4: Fill in personal information

After you choose the offer, fill in the necessary personal information.

- Anrede, Titel – Salutation, title

- Vorname – First name

- Nachname – Last name

- Postleitzahl, Ort – Postal code, city

- Straße, Hausnr. – Street, house no.

- Telefon-Nr. – Telephone no.

- Fax-Nr. – Fax no.

- E-Mail-Adresse – E-mail address

- Genaue derzeitige Berufsbezeichnung – Exact current job title

- Alter bei Versicherungsbeginn – Age at start of insurance

- 41 (Ihre Angabe aus der Eingabemaske) – 41 (your entry from the input mask)

- Geburtsdatum – Date of birth

- Datum wählen – Select date

- Staatsangehörigkeit Nationality

- Familienstand – Marital status

- Anrede Lebenspartner – Title of life partner

- Vorname Name Lebenspartner – First name Last name of partner

- Geburtsdatum Lebenspartner – Date of birth of life partner

Wrap Up

If you do not yet have private liability insurance in Germany, I can only recommend that you take out such insurance as soon as possible.

This protects you and your family and children from sometimes very high claims in case of damage.

So I hope that this summary has given you all the information you need to take out private liability insurance.

USEFUL INFORMATION ABOUT GERMANY

___

INSURANCE IN GERMANY

> 15 types of insurance in Germany any expat should have

___

FINANCES IN GERMANY

> Find Best Rates for Loan in Germany

___

UTILITIES IN GERMANY

> Cost of Home Utilities in Germany: Electricity, Gas, Heating, Water

___

WAGES AND TAXES IN GERMANY

> Tax return Germany – Everything you need to know

> Average Salary in Germany Latest Data

___

WORKING IN GERMANY

> CV in German with Europass: How to fill in step by step

___

LEARNING GERMAN LANGUAGE

> How to learn German fast: Top 10 strategies

* The links marked in this way are affiliate links and indicate that we receive a small commission, if you decide to buy the products or services offered by our partner sites. There’s no additional cost for you. Powered by TARIFCHECK24 GmbH.